What are bonds? Best Commodities Trading 2023

A bonds is a debt security, similar to an IOU. Borrowers issue bonds to raise money from investors willing to lend them money for a certain amount of time.

When you buy a bond, you are lending to the issuer, which may be a government, municipality, or corporation. In return, the issuer promises to pay you a specified rate of interest during the life of the bond and to repay the principal, also known as face value or par value of the bond, when it “matures,” or comes due after a set period of time.

Why do people buy bonds?

Investors buy bonds because:

- They provide a predictable income stream. Typically, bonds pay interest twice a year.

- If the bonds are held to maturity, bondholders get back the entire principal, so bonds are a way to preserve capital while investing.

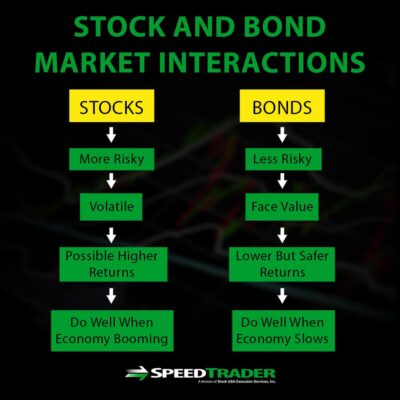

- Bonds can help offset exposure to more volatile stock holdings.

Companies, governments and municipalities issue bonds to get money for various things, which may include:

- Providing operating cash flow

- Financing debt

- Funding capital investments in schools, highways, hospitals, and other projects

What types of bonds are there?

There are three main types of bonds:

- Corporate bonds are debt securities issued by private and public corporations.

- Investment-grade. These bonds have a higher credit rating, implying less credit risk, than high-yield corporate bonds.

- High-yield. These bonds have a lower credit rating, implying higher credit risk, than investment-grade bonds and, therefore, offer higher interest rates in return for the increased risk.

- Municipal bonds, called “munis,” are debt securities issued by states, cities, counties and other government entities. Types of “munis” include:

- General obligation bonds. These are not secured by any assets; instead, they are backed by the “full faith and credit” of the issuer, which has the power to tax residents to pay bondholders.

- Revenue bonds. Instead of taxes, these are backed by revenues from a specific project or source, such as highway tolls or lease fees. Some revenue bonds are “non-recourse,” meaning that if the revenue stream dries up, the bondholders do not have a claim on the underlying revenue source.

- Conduit bonds. Governments sometimes issue municipal bonds on behalf of private entities such as non-profit colleges or hospitals. These “conduit” borrowers typically agree to repay the issuer, who pays the interest and principal on the bonds. If the conduit borrower fails to make a payment, the issuer usually is not required to pay the bondholders.

-

U.S. Treasuries

Are issued by the U.S. Department of the Treasury on behalf of the federal government. They carry the full faith and credit of the U.S. government, making them a safe and popular investment. Types of U.S. Treasury debt include:

- Treasury Bills. Short-term securities maturing in a few days to 52 weeks

- Notes. Longer-term securities maturing within ten years

- Bonds. Long-term securities that typically mature in 30 years and pay interest every six months

- TIPS. Treasury Inflation-Protected Securities are notes and bonds whose principal is adjusted based on changes in the Consumer Price Index. TIPS pay interest every six months and are issued with maturities of five, ten, and 30 years.

What are the benefits and risks of bonds?

Bonds can provide a means of preserving capital and earning a predictable return. Bond investments provide steady streams of income from interest payments prior to maturity.

The interest from municipal bonds generally is exempt from federal income tax and also may be exempt from state and local taxes for residents in the states where the bond is issued.

As with any investment, bonds have risks. These riskes include:

Credit risk:

The issuer may fail to timely make interest or principal payments and thus default on its bonds.

Interest rate risk:

Interest rate changes can affect a bond’s value. If bonds are held to maturity the investor will receive the face value, plus interest. If sold before maturity, the bond may be worth more or less than the face value. Rising interest rates will make newly issued bonds more appealing to investors because the newer bonds will have a higher rate of interest than older ones. To sell an older bond with a lower interest rate, you might have to sell it at a discount.

Inflation risk:

Inflation is a general upward movement in prices. It reduces purchasing power, which is a risk for investors receiving a fixed rate of interest.

Liquidity risk

This refers to the risk that investors won’t find a market for the bond, potentially preventing them from buying or selling when they want.

Call risk

The possibility that a bond issuer retires a bond before its maturity date, something an issuer might do if interest rates decline, much like a homeowner might refinance a mortgage to benefit from lower interest rates.

Avoiding fraud

Corporate bonds are securities and, if publicly offer, must register with the SEC. The registration of these securities can be verified using the SEC’s EDGAR system. Be wary of any person who attempts to sell non-registered .

Most municipal securities issued after July 3, 1995 are require to file annual financial information, operating data, and notices of certain events with the Municipal Securities Rulemaking Board (MSRB). This information is available free of charge online at www.emma.msrb.org. If the municipal bond is not fill with MSRB, this can be a red flag.