What is Fund Management?

Fund Management is the process in which a company that takes the financial assets of a person, company or another fund management company (generally this will be high net worth individuals). And use the funds to invest in companies that use those as an operational investment, financial investment or any other investment in order to grow the fund. Post which, the returns will be returned to the actual investor and a small amount of the returns are held back as a profit for the fund.

Explanation

Fund management is associated with managing the cash flows of a financial institution. The responsibility of the fund manager is to assess the maturity schedules of the deposits received and loans given to maintain the asset-liability framework. Since the flow of money is continuous and dynamic, it is of critical importance that asset-liability mismatch can be prevented. It is essential for the financial health of the entire banking industry to be dependent. Which in turn has an impact on the overall economy of the country.

For example, Fidelity manages $755 billion in U.S. equity assets under management. The responsibility of the fund manager is to assess the maturity schedules of the deposits received and loans given to maintain the asset-liability framework.

Fund Management also broadly covers any system which maintains the value of an entity. It applies to both tangible and intangible assets and is also referred to as Investment management.

Types of Fund Management

The kinds of Fund Management can be classified by the Investment type, Client type, or the method used for management. The various types of investments managed by fund management professionals include:

- Mutual Funds

- Trust Fund

- Pension Funds

- Hedge Fund

- Equity fund management

When classifying management of a fund by client, fund managers are generally personal fund managers, business fund managers, or corporate fund managers. A personal fund manager typically deals with a small quantum of investment funds, and an individual manager can handle multiple lone funds.

Offering Investment management services includes extensive knowledge of:

- Financial Statement Analysis

- Creation and Maintenance of Portfolio

- Asset Allocation and Continuous Management

Who is a Fund Manager?

A fund manager is essential for the management of the entire fund under all circumstances. This manager is entirely responsible for strategy implementation of the decided fund and its portfolio trading activities. Finding the right fund management professional usually requires Trial and Error combined with specific aid from investors in a similar position.

Generally, the investor will permit a fund manager to handle a limited fund for a specified period to assess and measure the success in proportion to the growth of the investment property.

Fund management uses its means of making decisions with ‘Portfolio Theory’ applicable to various investment situations. A fund manager can also use multiple such theories for managing a fund, especially if the fund includes multiple types of investments. The managers are paid a fee for their work, which is a percentage of the overall ‘Assets under Management.’

The qualifications required for a position in a fund management institution consist of a high level of educational and professional credentials such as a Chartered Financial Analyst (CFA) accompanied with appropriate practical investment managerial experience. Which is generally decision making in portfolio management. Investors are on the look-out for consistent and long-term fund performance, whose duration with the fund shall match with its performance period.

Responsibilities of the Fund Manager?

The fund manager is the heart of the entire investment management industry responsible for investing and divesting of the investments of the client. The responsibilities of the fund manager are as below:

#1 – Asset Allocation

The class of asset allocations can be debated, but the standard divisions are Bonds, Stocks, Real estates, and Commodities. The type of assets exhibits market dynamics and a variety of interaction effects, which allocate money amongst various asset classes leading to a significant impact on the targeted performance of the fund. This aspect is very critical as the endurance of the fund in challenging economic conditions will determine its efficiency and how much return it can garner over some time under all circumstances.

Any successful investment relies on the asset allocations and individual holdings for outperforming specific benchmarks such as bond and stock indices.

#2 – Long-term Returns

It is essential to study the proofs of the long-term returns against various assets and holding period returns (returns accruing on average over multiple lengths of investment). For example, investments spread across a very long maturity period (more than ten years) have observed equities generating higher returns than bonds and bonds, generating greater returns than cash. This is due to equities being more risky and volatile than bonds, which are more dangerous than money.

#3 – Diversification

Going hand in hand with asset allocation, the fund manager must consider the degree of diversification, which applies to a client under their risk appetite. Accordingly, a list of planned holding will have to be constructed deciding what percentage of the fund should be invested in a particular stock or bond. Adequate diversification requires the management of the correlation between the asset and liability return. Internal issues about the portfolio, and cross-correlation between the returns.

What are Fund Management Styles?

There are various fund management styles and approaches:

#1 – Growth Style

The managers using this style have a lot of emphasis on the current and future Corporate Earnings. They are even prepared to pay a premium on securities having strong growth potential. The growth stocks are generally the cash-cows and are expected to be sold at prices in the northern direction.

Growth managers select companies having a strong competitive edge in their respective sectors. A high level of retained earnings is the expectation for such scripts to be successful as it makes the Balance Sheet of the firm very strong to attract investors. This can be coupled with a limited dividend distributed and low debt on the books, making it a definite pick by the managers. The scripts which are part of such a style will have a relatively high turnover rate since they are frequently traded in large quantities. The returns on the portfolio are made up of Capital gains resulting from stock trades.

The style produces stunning results when markets are bullish. But the portfolio managers are required to show talent and flair for achieving investment objectives during downward spirals.

#2 – Growth at Reasonable Price

The Growth at Reasonable Price style will use a blend of Growth and Value investing for constructing the portfolio. This portfolio will usually include a restricted number of securities that are showing consistent performance. The sector constituents of such portfolios could be slightly different from that of the benchmark index. To take advantage of growth prospects from these selected sectors since their ability can be maximized under specific conditions.

#3 – Value Style

Managers following such a response will thrive on bargaining situations and offers. They are on the hunt for securities that are undervalued about their expected returns. Securities could be undervalued even because they do not hold preference with the investors for multiple reasons.

The managers generally purchase the equities at low prices and tend to hold them till they reach their peak. Depending on the time frame expected, and hence the portfolio mix will also stay stable. The value system performs at its peak during the bearish situation, although managers do take the benefits in conditions of a bullish market. The objective is to extract the maximum benefit before it reaches its peak.

#4 – Fundamental Style

This is the basic and one of the most defensive styles which aim to match the returns of the benchmark index by replicating its sector breakdown and capitalization. The managers will strive to add value to the existing portfolio. Such styles are generally adopted by mutual funds to maintain a cautious approach since many retail investors with limited investments expect a necessary return on their overall investment.

Portfolios managed according to this style are highly diversified and contain a large number of securities. Capital gains are made by underweighting or overweighting specific securities or sectors, with the differences being regularly monitored.

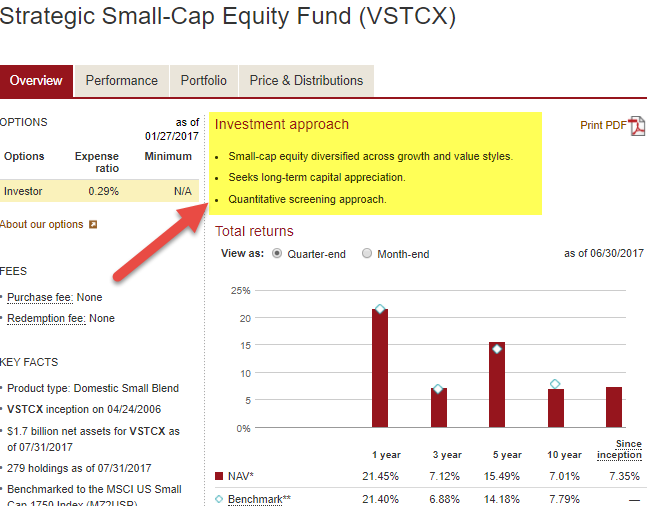

#5 – Quantitative Style

The managers using such a style rely on computer-based models. That track the trends of price and profitability for identification of securities offering higher than market returns. Only necessary data and objective criteria of protection are taken into consideration. And no quantitative analysis of the issuer companies or its sectors are carried out.

#6 – Risk Factor Control

This style is generally adopted for managing fixed-income securities which take into account all elements of risk such as:

- Duration of the portfolio compared with the benchmark index

- The overall interest rate structure

- Breakdown of the deposits by the category of the issuer and so on

#7 – Bottoms-Up Style

The selection of the securities is based on the analysis of individual stocks with less emphasis on the significance of economic and market cycles. The investor will concentrate their efforts on a specific company instead of the overall industry or the economy. The approach is the company exceeding expectations despite the sector or the economy not doing well.

The managers usually employ long-term strategies with a buy and hold approach. They will have a complete understanding of an individual stock and the long-term potential of the script and the company. The investors will take advantage of short-term volatility in the market for maximizing their profits. This is done by quickly entering and exiting their positions.

#8 – Top-Down Investing

This approach of investment involves considering the overall condition of the economy. And then further breaking down various components into minute details. Subsequently, analysts examine different industrial sectors for the selection of those scripts which are expected to outperform the market.

Investors will look at the macroeconomic variables such as:

- GDP (Gross Domestic Product)

- Trade Balances

- Current Account Deficit

- Inflation and Interest rate

Based on such variables, the managers will reallocate the monetary assets for earning capital gains rather than extensive analysis of a single company or sector. For instance, if economic growth is doing well in South East Asia compared to the domestic development of the EU (European Union), investors may shift assets internationally by purchasing Exchange-traded funds that track the targeted countries in Asia.